How to make an invoice

admin2024-01-10T05:23:39+00:001. What is an invoice?

Let’s start with the basics, answering the question: what is an invoice?

An invoice is a commercial document that contains the information relating to a transaction or purchase or sale of goods or services.

When you consider how to issue an invoice, the first thing you should know is that the applicable regulation is the Invoicing Regulation and that, in accordance with it, freelancers and SMEs must issue invoices for each job carried out. Further information on this subject is provided below.

2. How to issue an invoice?

The traditional system was the paper invoice sent by post or delivered to the customer’s premises, often handwritten on a paper invoice book or printed on matrix paper.

With the development of business computers, invoices made in word or excel became widespread and were often sent to the customer in PDF format via email.

In our Google Drive templates you can download a free excel spreadsheet invoice template that will serve as a basis for customising your own invoices.

Elements to include when creating an invoice:

Number and, if applicable, series. The numbering of the invoices within each series will be correlative. There may be separate series in the following cases: several establishments, operations of a different nature or corrective invoices. Normally a new series is started for each year.

The date of issue.

Name and surname, full name or company name, both of the person obliged to issue the invoice and of the customer or recipient of the operations.

Tax identification number attributed by the Spanish Administration (NIF) or, where applicable, by that of another Member State of the European Union, with which the person obliged to issue the invoice has carried out the transaction.

Address, both of the person obliged to issue the invoice and of the recipient of the transactions.

Description of the transactions, including all the data necessary to determine the taxable amount of the tax, i.e. the total amount of the consideration, corresponding to the transactions and their amount, including the unit price excluding tax of the said transactions, as well as any discount or rebate not included in the said unit price.

The rate of VAT and the equivalence surcharge, if applicable, as well as the percentage of personal income tax withholding, if applicable, as in the case of professionals.

The amount of tax to be charged, if any, which must be entered separately.

The total amount to be paid.

The date on which the transactions documented were carried out or on which, where applicable, the advance payment was received, provided that this is a date other than the date of issue of the invoice.

3. When should we issue an invoice?

It is not only a question of knowing how to issue an invoice, but also of knowing when you are obliged to do so. As an entrepreneur or self-employed professional, you are obliged to issue and deliver invoices, or other supporting documents, for the transactions you carry out in the course of your activity.

Don’t forget that you must always keep a copy of the document you issue. In other words, you must be registered with the tax authorities in order to issue invoices.

You are also obliged to keep all the invoices you receive from other business people or professionals.

It is compulsory for the supply of goods and services to issue and keep the invoices containing the VAT transactions involved in your activity (the obligation also extends to those that are not subject to the tax and those that are subject to the tax but exempt) and likewise if you are covered by a special VAT regime.

However, in some special VAT regimes, in principle it is not necessary to issue invoices, giving rise to the following exceptions that mainly affect transactions with private individuals:

VAT-exempt transactions (not to be confused with transactions not subject to VAT).

Those carried out by entrepreneurs or professionals under the special equivalence surcharge regime.

Those carried out by business people or professionals under the simplified VAT system, unless the VAT due is determined on the basis of the volume of income.

Those carried out by business people or professionals in the special regime for agriculture, livestock and fishing.

You are always obliged to issue an invoice when the recipient is a businessperson or professional acting as such and when your client requires it in order to exercise any tax right.

On these occasions it is advisable to check the specific case with an advisor.

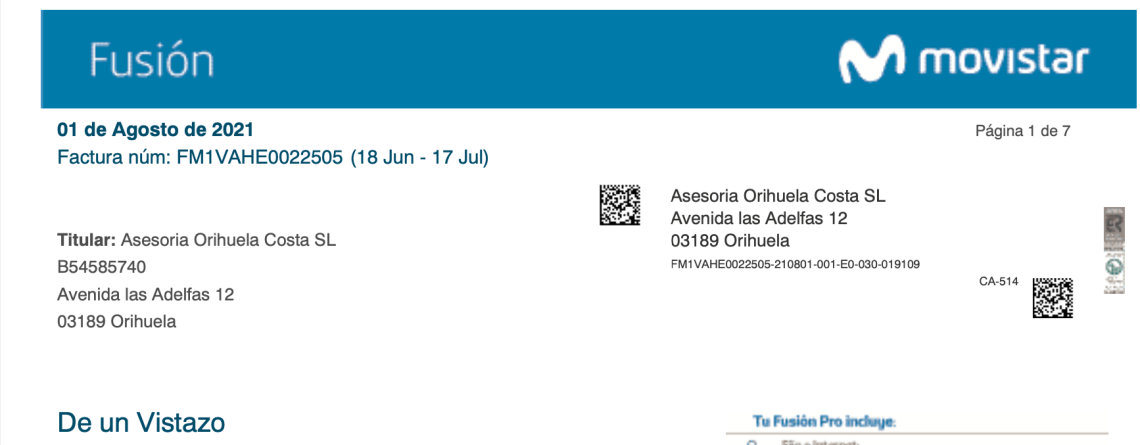

4. Let’s look at an example of an invoice

Let’s take an example of an invoice. A self-employed professional provides computer maintenance services and issues an invoice to a company.

The date the work is carried out is the same as the date the invoice is issued and collected.

The cost of the invoice is constructed from the unit price per hour worked.

To the gross amount of your work, 21% VAT is added and, if applicable, the IRPF deduction is subtracted. In this case, as you are a self-employed professional, a deduction of 15% should be applied.

The VAT settlement of the invoice corresponds to the self-employed worker and the IRPF withholding corresponds to the company receiving the invoice.

Here is an example of an invoice.

5. What is the deadline for sending an invoice?

Invoices or substitute documents must be issued at the time the transaction is carried out.

However, when the recipient of the transaction is a businessperson or professional acting as such, they must be issued within a period of one month from the aforementioned moment.

In any case, the invoices or replacement documents must be issued before the 16th day of the month following the tax assessment period in the course of which the transactions were carried out.

6. The simplified invoice and the ticket

Since the entry into force of the Invoicing Regulation currently in force, the simplified invoice has replaced the ticket, which until then was allowed for transactions of up to 3,000 euros including VAT in activities such as retail sales, the hotel and catering industry and passenger transport (taxis), among others.

Since then, any self-employed person may issue simplified invoices for transactions of up to 400 euros, including VAT.

7. Electronic invoicing

It has been clear for some time now that electronic invoicing is the prevailing invoice model, definitively displacing paper invoices and invoices in Excel or Word.

In fact, the invoicing regulation grants the same treatment to electronic invoices as to paper invoices. Moreover, it is compulsory for suppliers to the Public Administration and large companies to use them.

8. What happens if I am asked for a duplicate invoice?

In principle, you can only issue one original of each invoice or substitute document. However, you are allowed to issue duplicates, on which the expression “duplicate” must appear, which will have the same effectiveness as the original invoice or substitute document, in two cases:

When several recipients are involved in the same delivery of goods or provision of services. In this case, the portion of the taxable base and the tax charged to each of them must be stated on the original and on each of the duplicates.

In the event of loss of the original for any reason.

9. What other types of invoice are there?

Apart from the ordinary, simplified and electronic invoices mentioned above, you should be aware of other important types of invoice.

We have an article in which we describe each type in detail, which you can consult by clicking here. But as a compilation:

Corrective invoice

The corrective invoice is used when a correction has to be made to a previous invoice. Either because it does not meet the requirements established by Law, or because products, containers or packaging are returned, or because discounts or rebates are given after the operation.

It must also be used in the event of a final decision that renders ineffective or modifies the operations carried out, and in the event of the declaration of bankruptcy of the recipient of the invoice.

It must be issued as soon as the reasons for issuing it are known, and provided that no more than four years have passed since the invoice to be rectified was issued.

Recapitulative invoice

The recapitulative invoice makes it possible to include in a single invoice several operations addressed to the same recipient and which fall on different dates, but in the same calendar month.

When the recipient of the transaction is a businessperson or professional acting as such, the invoice must be issued before the 16th day of the month following the month in which the transactions were carried out.

Proforma invoice

The purpose of this document is to provide information on a commercial offer, indicating the products or services that the seller will provide to the buyer at a certain price, so that the buyer has as much information as possible on the future purchase to be made.

It has no accounting value and does not serve as a receipt, so it is not numbered, nor is it advisable to sign or stamp it, unless the client explicitly requests it.

From Asesoría Orihuela Costa we hope that, with all this information, you will be able to keep the accounts of your business by yourself, and we offer you the help of our invoicing software to ease the way of bookkeeping, which is often quite tedious.