")

In January of each year, offer your employees the opportunity to fill out a new Form 145 to indicate whether their family or personal circumstances have changed and the withholding rate applied to their payroll needs to be modified.

Form 145 is a document used in Spain to communicate relevant data on personal income tax withholding to the company or payer.

Correctly completing it ensures that the appropriate withholdings are applied according to the personal and family situation of the taxpayer.

This form is essential in tax administration, as it allows withholdings to be adjusted to the economic reality of the employee.

Throughout the article, its characteristics, use and procedure for its correct presentation will be explored.

What is form 145?

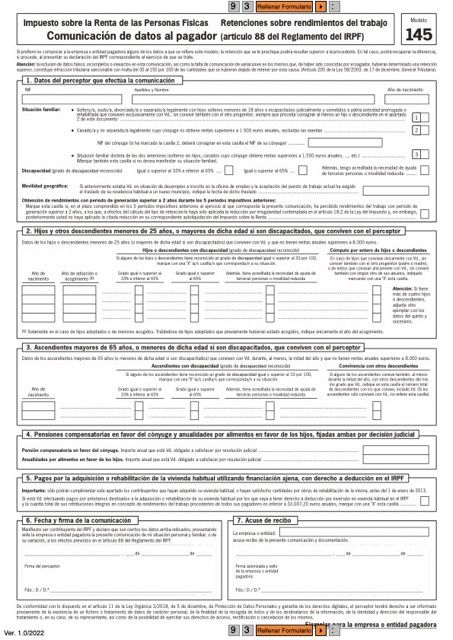

Form 145 is a key document in the Spanish tax field. It is used to provide information related to the withholding of Personal Income Tax (IRPF).

Its correct completion is essential for the proper tax management of workers.

Definition and objective

This form is a form that workers and employees of a company must submit to inform their payer, usually the company in which they work, about their personal and family situation.

Its main objective is to establish the type of withholding that will be applied to the salary or remuneration of the worker, thus ensuring that current tax regulations are respected.

Form 145 also plays a crucial role in facilitating the adaptation of tax withholdings to the particular circumstances of each worker.

This implies that factors such as family situation, the number of dependent children or any other relevant situation influence the amount that will be withheld from their salary.

Importance of Form 145 for tax administration

The correct use of Form 145 has a significant impact on tax administration.

By providing accurate information, transparency in the tax field is increased and it is ensured that the withholdings applied to workers’ payrolls are appropriate.

This also helps to avoid conflicts between taxpayers and the Tax Agency, thus reducing the risk of sanctions.

From an administrative point of view, this model allows the Tax Agency to have better control over the withholdings made in the labor field.

Organizations that correctly comply with their tax obligations, including the presentation of Form 145, contribute to the proper functioning of the Spanish tax system.

On the other hand, variations in the personal circumstances of taxpayers, as well as their changes in employment, make the presentation of this model a necessary and continuous practice throughout working life.

By keeping up to date with these variations, greater equity in the tax obligations of citizens is facilitated.

IRPF withholdings for form 145

Income tax withholdings are a fundamental part of the Spanish tax system.

They refer to the amounts that are deducted from workers and self-employed persons on their earnings to anticipate the payment of income tax.

Below, we detail how these withholdings are linked to Form 145.

How Form 145 affects Income Tax

Form 145 is the document that allows taxpayers to communicate to their payers the data necessary to calculate the withholding that must be applied to them.

This includes information about their personal and family situation, which can modify the percentage of the withholding.

An important aspect is that the data provided in Form 145 determines whether a higher or lower withholding is applied depending on the particular situation of the taxpayer.

When a worker presents Form 145, they are enabling their payer to adjust the withholdings to suit them.

This means that if a taxpayer has changes in his or her marital status, such as marriage or the birth of children, he or she may benefit from a reduced withholding rate.

This, in turn, can result in greater purchasing power throughout the year.

Applicable withholding rates

There are several types of withholdings that may be applicable depending on the circumstances of each taxpayer.

These withholding rates are linked to aspects such as total income, personal and family situation, and the nature of the income.

Some of the most common types are:

Withholdings for work income

These are applied to the salaries and wages of employees. They are conditioned by the level of income, as well as family burdens.

Withholdings for income from economic activities

Applicable to self-employed workers and professionals who must comply with the direct estimate or objective estimate regime. The withholding percentage varies according to the type of activity and annual income.

Withholdings on dividends or interest

These are applied to income obtained from financial investments, such as dividends, interest or capital gains, and have a fixed rate, subject to regulatory changes.

Therefore, understanding the applicable withholdings and how they relate to Form 145 is essential for correct management of tax obligations.

Filing the form allows obtaining withholdings adjusted to the taxpayer’s reality and facilitates tax planning throughout the year.

Withholdings from workers

When hiring a new employee, it is important that your company makes them fill out Form 145, so that the employee can report their personal and family situation in order to calculate the applicable withholding rate.

However, if there are later changes in the personal and family situation of the affected employee and they communicate them to the company, the withholding rate must be modified.

Therefore, it is advisable that in January of each year you offer your employees the possibility of filling out a new Form 145 reporting the changes that occurred in the previous year and that they have not yet communicated.

Circumstances that influence withholdings

For these purposes, remember some of the personal and family circumstances that allow workers to pay less tax on their personal income tax and that, therefore, influence the withholding rate that is applicable to them:

- The number of descendants or their personal circumstances (disability), to the extent that this influences the personal and family minimum applicable to their personal income tax.

- The obligation to pay a compensatory pension to the spouse, or annual alimony payments for the children, which allows for certain reductions.

- Other circumstances that may affect the withholding are that the spouse does not receive non-exempt annual income exceeding 1,500 euros, having dependent ascendants, or applying the deduction for the purchase of a habitual residence and having work remuneration less than 33,007.20 euros.

Employee who does not file Form 145

If the employee does not want to reveal his personal situation (neither at the time of being hired, nor later) and does not file Form 145, his company must calculate his withholding rate as if he were single and without family or other responsibilities (that is, as if he were not entitled to any incentive in the IRPF).

Update of the Withholdings of model 145

For the purposes of calculating withholdings, check the forms 145 submitted by your employees. In this regard:

- If an employee’s circumstances have not changed with respect to the previous year, it is not necessary to submit form 145.

- If an employee submits a form 145 with data that are not true (for example, that his spouse does not earn income) in order to benefit from a lower withholding, calculate his withholding according to the data provided. In any case, warn them that it is they who will be responsible to the Tax Authorities

- And if you do not have a worker’s 145, calculate their withholding considering that their family situation is 3 (single) and that they have no dependent children or ascendants.

In January, ask your employees to provide you with the updated form 145.

Offering your employees the option of filing Form 145 every January is beneficial for everyone:

- For your company, this will mean that fewer employees will have to report changes that took place in the previous year at a different time (for example, mid-year, which would force you to recalculate the withholding rate established in January).

- For employees, if the changes reported in Form 145 result in a lower withholding rate, this will allow them to receive a higher net amount each month; and if they result in an increase, they will avoid the penalties that the Treasury may impose on them for not reporting these changes.

Incorrect data

If any of your employees includes incorrect data in order to support a lower withholding (for example, declaring that their spouse does not earn income, or that they have dependents who are not true), they – and not the company – will be responsible to the Treasury.

If the employee is required to file a personal income tax return, the Treasury may impose a penalty of 35% of the amounts not withheld (150% if not required).

Keep Form 145

Always calculate the withholding based on the data provided by your employees (even if you know they are incorrect), and keep the signed Form 145.

This way, in the event of an audit, your company will be able to prove that it has acted correctly.

Keep Form 145 submitted by employees and calculate the withholdings based on the data provided by them. It is the employees who are responsible to the Treasury for any inaccuracies they make when filling out this form.

Problems with model 145

The problem with Form 145 and withholdings arises when we work for 2 companies and we submit Form 145 to one company independently of the information from the other company.

Each company withholds based on the salary you will receive from that company but does not know what salary you will receive from the other company.

If this is your case, you will almost certainly have to pay in your income tax return.

This is solved by adding the 2 figures and telling both companies.

Data of the recipient and payer of model 145

Correct completion of the recipient and payer data is essential for the proper functioning of Form 145.

This information allows the Tax Authority to accurately manage withholdings and ensure that the taxpayer’s real situation is reflected.

Required information

When completing Form 145, it is important to provide specific information about both the recipient and the payer. This data is necessary for the correct identification and management of tax withholdings. The main data that must be included are:

- Recipient data:

- Name and surname.

- Identification number: DNI,

- NIE or passport.

- Personal and family situation.

- Tax address.

- Payer data:

- Name or corporate name of the company or entity.

- NIF (Tax Identification Number).

- Full address of the payer.

Changes in the recipient’s data

It is essential that any change in the recipient’s data is updated by submitting Form 145.

This ensures that the withholdings are adjusted to the taxpayer’s current situation, avoiding future problems with the Tax Agency.

Change in personal or family situation

Any change in the recipient’s personal or family situation must be communicated to the company or payer through Form 145. This includes changes such as:

- Modifications in marital status (single, married, divorced).

- Changes in the number of children or dependents in charge.

- Disability or dependency situations.

These changes can directly affect the type of withholding applied to personal income tax, so it is crucial to keep the information up to date.

Change of employer

When a recipient changes employer, a new Form 145 must be submitted to reflect this change.

It is important that the new payer has all the updated information about the recipient, including:

- Updated personal data.

- The new personal and family situation of the worker.

- Other relevant data that may influence the withholdings.

This procedure is essential to ensure that the withholdings are calculated appropriately and that current tax regulations are complied with.

How to fill out form 145

Filling out Form 145 is an essential task to ensure that the IRPF withholdings are correct.

This process can be simple if the appropriate guidelines are followed. Below are the steps required to complete the form correctly.

Step by step to complete Form 145

Section 1: Personal data

The first part of the form requires the entry of the personal data of the recipient. The following information must be provided:

- Name and surname

- Tax identification number (NIF)

- Full address

- Postal code

- Contact telephone number

It is important that all data is entered without errors, as it can influence the correct withholding of the tax.

Any discrepancy can lead to problems in the future.

Section 2: Personal and family situation

In this section the taxpayer must detail his or her personal and family situation, which directly affects the percentage of the IRPF withholding.

The information to be included is:

- Marital status

- Number of children or descendants

- Disability status, if applicable

- Other dependent ascendants

The inclusion of this information is key, since family and personal burdens can modify the applicable withholdings and the corresponding tax rate.

Section 3: Incompatibilities

This section refers to possible incompatibilities that may affect the withholding declaration.

Generally, it must be indicated whether the recipient has other income or withholdings from different payers.

The following must be considered:

- Is the recipient a pensioner?

- Does he/she receive income from other economic activities?

It is essential to be thorough in this section, since it may affect the person’s tax status in the corresponding fiscal year.

Section 4: Signature and date

Finally, it is necessary to sign and date the document. The signature certifies that the data entered is true and that the taxpayer is responsible for the information declared. This section requires:

- Signature of the recipient

- Date of completion of the form

It is vital that this section is complete, since a signed form lacks administrative validity without the corresponding date.

Tools and resources available for form 145

Fillable PDF version

Form 145 is available in fillable PDF format. This format allows you to work with the document digitally, making it easier to complete.

It can be downloaded from the official website of the Tax Agency. Using a digital version helps to avoid typing errors and facilitates document management.

Instructions on the Tax Agency website

The Tax Agency offers detailed instructions on how to complete form 145. These guides are available on its website and can be consulted to resolve doubts related to specific fields or additional requirements. Accessing these instructions is recommended to ensure the correct presentation of the form, thus avoiding possible inconveniences.

Filing and declaring income tax

Filing Form 145 is a fundamental part of the income tax declaration process, as it establishes the withholdings that will be applied to the taxpayer’s income. The deadlines and their relationship with the annual declarations are detailed below.

Deadlines for filing Form 145

Form 145 should preferably be filed when an employment relationship begins or when significant changes occur in the employee’s personal situation that may affect their withholdings. However, it is important to take into account certain specific deadlines:

- The form is prepared before the first payroll in which the adjusted withholdings will be applied.

- If there are changes in the information that affects the form, it must be filed within a period that allows the company to make the changes to the corresponding withholdings, ideally in the same month in which these changes occur.

- If it is not filed within the established time, the employee could be affected by incorrect withholdings, which may lead to adjustments in the annual income tax return.

Annual declarations and their relationship with Form 145

Annual income tax declarations are closely related to what has been declared and withheld through Form 145. These are some aspects to consider:

- The withholdings applied to payrolls throughout the year must be reflected in the annual income tax declaration, where it will be verified whether the withholding has been sufficient or whether an additional payment must be made.

- It is possible that, after the annual declaration, the taxpayer will receive a refund if there has been an excess in the withholdings applied in relation to the total of their taxable income.

- Form 145 is submitted to the company, which is responsible for managing the withholdings, while the annual declaration is the responsibility of the employee, who will review their entire tax situation accumulated during the year.

Therefore, it is crucial that both the presentation of Form 145 and the subsequent income tax declaration are carried out as accurately as possible to avoid problems with the Tax Administration. The correct management of these documents and deadlines will contribute to better tax planning and avoid surprises at the time of filing.

Special cases of Form 145

There are particular situations in the area of withholdings that can influence the filing of Form 145.

These special cases cover aspects related to family composition, the age of taxpayers and situations of dependency, among others.

Large families and disability situations

Large families, as well as those with a disabled person, can benefit from certain deductions and considerations in Form 145.

These circumstances can affect the withholding of personal income tax by generating a right to reductions in the tax base.

- Large families: Those with three or more children can access tax deductions that reduce the tax burden.

- Disability situation: Family members who have a recognized disability can also opt for additional deductions, thus facilitating the management of their tax obligations.

It is essential that families in these situations report their status on Form 145 in order to benefit from these tax advantages.

People over 65 years of age and dependent ascendants

People over 65 years of age have preferential tax treatment, which is reflected in Form 145.

Taxpayers in this age group can enjoy a greater reduction in personal income tax withholdings.

- Taxpayers over 65 years of age: This category benefits from a greater exemption, which can result in lower tax withholdings.

- Dependent ascendants: If a taxpayer has dependent ascendants in their care, they can also opt for additional tax deductions, since these circumstances increase family burdens.

These data are relevant to ensure that the personal situation is adequately reflected in the tax return, allowing the withholding to be adjusted fairly.

Annuities for alimony and child support

Annuities for alimony, whether for children or other persons, have a specific treatment in Form 145.

These amounts can influence the IRPF withholding and it is important to declare the situation correctly.

- Annuities for children: The amounts received as alimony can be deducted, which affects the tax withholding.

- Alimony: In cases where alimony is paid to third parties, such contributions are considered in the declaration and may be relevant for the determination of withholdings.

Properly declaring these annuities allows for proper management of the tax burden and ensures that the taxpayer does not pay more than what he or she should.