")

Getting a mortgage can be a complicated process. There are several tricks and strategies to increase the chances of a successful application, ranging from managing savings to preparing the necessary documentation.

It is essential to understand the importance of prior savings, job stability, and maintaining a good credit history.

These factors are crucial when financial institutions evaluate a mortgage application.

Why do we need money?

The new social media pseudo-advisors advise not to take out loans, to live and be happy with what you have.

I am of the opinion that living with what you have is practically impossible. Unless you are a millionaire and obviously you are not reading this post.

I remember when I was young talking to a famous businessman from Torrevieja, showing him my doubts about loans, because I was studying financial mathematics in my economics degree in Alicante, and I showed him my financial (and existential) doubts about borrowing money from banks.

And he told me, look PATRICK I have borrowed from banks all my life and look at me, here I am.

Human beings are programmed to survive, but they also want to live better.

Wanting to live better, to improve, to grow, is what leads to success.

And if you want to live better and grow, you need money, unless you are the inventor of the future iPhone, you need to borrow that money.

Now, there are many kinds of loans, you can borrow it from your family, you can borrow it from a friend. But what if your family or friends have no resources?

You have to turn to a bank.

And this is where the complications begin.

Importance of pre-mortgage savings

Saving before applying for a mortgage is essential to present a solid profile to financial institutions.

Saving not only covers the down payment, but also demonstrates responsibility and financial management skills, which are highly valued by lenders.

demonstrates responsibility and financial management skills, factors that are highly valued by lenders.

Reasons to have significant savings

Having significant savings is essential for several reasons:

- Reduction of the amount to be financed: By having considerable savings, you can cover the down payment required by the bank, which is usually 20% of the value of the home.

- Better conditions: Having savings can make it easier to obtain better interest rates and more favourable loan conditions.

- Demonstration of stability: A history of savings reflects financial management skills and responsibility, which is a plus for banks.

How to calculate how much money you need to save

To determine how much money to save, several factors need to be considered:

- Price of the property: Knowing the exact cost of the property helps to set a savings target.

- Down payment percentage: Generally, 20% of the total value is required for the down payment, as well as an additional 10% to cover associated costs (notary, taxes, etc.).

- Contingencies: It is advisable to have an additional margin in savings to deal with unforeseen events during the purchase process.

For example, if you want to buy a house with a price of 300,000 euros, you should calculate a saving of approximately 90,000 euros to cover the down payment and additional expenses.

Watch this video on how to download a working life

Job stability and its impact on mortgages

What the bank wants is for you to demonstrate that you are going to be able to pay back their money, with interest…

Job stability is a determining factor in the process of demonstrating your ability to repay a mortgage.

Lenders analyse the employment history of applicants to assess their financial risk and ability to repay.

It is clear that your work history is a reflection of your personality and your profile.

If your working life reflects constant job changes or short periods of work, you are an unstable or conflictive person.

How to prove job stability to banks

To demonstrate employment stability, it is essential to provide documentation that supports the duration and nature of employment. This includes:

- Employment contracts indicating the type of employment, either permanent or temporary.

- Pay slips for the last few months showing regular income.

- Employment history that certifies seniority and current employment situation.

A stable employment profile increases the bank’s confidence in the applicant’s ability to meet the monthly mortgage payments.

Advantages of a permanent contract

Having a permanent contract is viewed positively by financial institutions. Some of the advantages include:

- Greater long-term security, which means stable income.

- Lower risk perception by lenders.

- Ease of access to better mortgage conditions.

Options for the self-employed and eligibility

The self-employed face certain challenges when applying for a mortgage, as their employment situation may be less stable. In order to access financing, they must meet certain requirements, such as:

- Demonstrate consistent income for at least two years.

- Submit income tax returns and other tax documents.

- Have a viable business plan that supports the economic activity.

In this way, the self-employed can increase their chances of obtaining the desired loan by showing that they have solid financial resources and a stable business track record.

Did you know that married men with two children have a better banking profile than a single man without children?

Credit history and its influence

The credit history is a crucial element in the mortgage approval process.

It reflects a person’s financial behaviour, determining his or her ability to repay debts.

A good credit history can open doors to better loan conditions.

Tips for maintaining a good credit history

To ensure a favourable credit history, it is essential to follow certain guidelines.

Maintaining timely payments is key.

Late payments can seriously affect your score.

This includes not only loan repayments, but also utility bills and credit cards.

- Use credit responsibly.

- Limit the use of credit to a low percentage of the available limits.

- Avoid opening too many accounts at once.

Tools to check your credit history

Accessing tools that allow you to check your credit history is essential.

Many banks and financial institutions offer services for users to check their situation.

There are platforms that allow you to check your credit report for free or at a reduced cost.

- Request a credit report free of charge from reputable institutions.

- Use applications that monitor your credit score.

Actions to improve your credit score

There are several actions that can be taken to improve your credit rating.

Paying off existing debts and keeping credit card balances low can have a positive impact.

It is also advisable to correct errors in the credit report that can hurt the score.

- Consolidate debts to make them easier to manage.

- Consult a financial advisor if necessary.

- Always respect the established payment deadlines.

Use of collateral and guarantees for your mortgage?

The use of guarantors and guarantees is a strategy that can make it easier to obtain a mortgage.

Banks love guarantors, it is logical, a guarantor is a person who gives a banking profile, different from yours and who satisfies the bank to lend you the money.

By having the backing of a third party, the risk perceived by financial institutions is reduced, which can improve the conditions of the loan.

Benefits of having a guarantor

Having a guarantor offers multiple advantages in the mortgage application process. The main benefits include:

- Increased reliability: The presence of a creditworthy guarantor can provide greater security to the lender.

- Better terms: Banks typically offer lower interest rates and more flexible terms when a guarantor is involved.

- Access to larger amounts: By reducing the risk for the bank, higher amounts of financing can be obtained.

- Possibility of approval in complicated cases: A good guarantor can be the determining factor in the approval of mortgages for applicants who would otherwise be rejected.

Associated risks for the guarantor

Despite the benefits, being a guarantor carries certain risks that should be carefully considered. Some of these include:

- Financial liability: If the borrower defaults on payments, the guarantor will be liable for the debt, which can impact their financial situation.

- Impact on credit history: A default can negatively affect the guarantor’s credit history, making future credit applications more difficult.

- Personal relationships: In many cases, guarantors are family members or friends, which can create tensions if payment problems arise.

Mortgage pre-approval process

The mortgage pre-approval process is an essential step in applying for a mortgage.

It allows applicants to know in advance the conditions offered by the bank and facilitates the preparation for obtaining the loan.

Keep in mind that the person in charge at the bank will not be the person who finally approves your loan.

But he or she will have a personal opinion about you and will treat you well, be polite, be punctual and diligent.

This will give her confidence and put her on your side.

Steps to obtain mortgage pre-approval

Obtaining a mortgage pre-approval requires following a series of steps to ensure that the bank properly assesses the applicant’s financial situation.

These steps include:

- Gathering the necessary documentation, such as IDs, proof of income and bank statements.

- Make an appointment with the bank or mortgage lender to discuss pre-approval. Banks have mortgage brokers, who are very professional, so don’t try to fool them.

- Present documentation and provide detailed information about your personal financial situation. If you are a customer, your bank statement already reflects how you manage your money. If you are not a customer, you will be asked about everything.

- Wait for the bank’s assessment, where your income, credit history and existing debts will be analysed. In principle, at the first appointment, the mortgage officer will be able to tell you whether your mortgage is pre-approved.

Advantages of being pre-approved

Having a mortgage pre-approval has multiple benefits. Among them are the following:

- Knowing the maximum amount that can be requested, which helps to define the budget for the purchase of the home.

- Increase credibility with sellers, as it demonstrates that the buyer has the necessary financial backing.

- Facilitate the official mortgage application process by having all the documentation ready and a preliminary analysis done by the bank.

The golden rule of mortgages: 35%.

The 35% figure is magic.

If at the end of subtracting from your income, all of your loan expenses, debts and living expenses and incidentals, if the money you have left is 35% of your total income, you will probably be approved for a mortgage.

Compare mortgage offers

Who hasn’t heard the saying: always ask for two quotes?

When asking for a mortgage it is essential to ask for a minimum of two banks, because even if they don’t know you, the bank may be in a situation of financial expansion and have better conditions than your old bank.

And applying for a loan does not cost money (if you are granted it, yes).

Comparing mortgage offers is a crucial step in securing the best financing.

Different entities offer conditions that can vary significantly, so making a good comparison allows you to find the most favourable options.

Keys to find the best mortgage offer

In order to detect the best mortgage offer, it is important to consider several factors. Among them are:

- Interest rate: Analyse whether the mortgage has a fixed or variable rate, as well as the revision conditions.

- Fees: Pay attention to possible opening, early cancellation or management fees.

- Repayment period: Assess how long the loan is expected to take to repay, as this influences the total interest.

- Additional links: Consider whether the mortgage is linked to products such as insurance or accounts that may make the offer more expensive.

Using a mortgage advisor to improve your options

Brokers are not well known in Spain, but there are some.

We recommend Viva Home Credit, a block registered in Spain which has its office in the Los Dolses shopping centre.

Karine, the owner is a woman who has worked in banking for a long time and knows all the secrets of taking out a mortgage or a loan.

Having the support of a mortgage advisor can make it easier to find the best deal. These professionals have in-depth knowledge of the market and offer several advantages:

- Access to multiple entities: An advisor can help you access exclusive offers that are not available to the general public.

- Negotiating terms: Their expertise allows them to negotiate better terms and interest rates on behalf of the client.

- Personalised analysis: They provide an analysis tailored to the particular financial situation, guiding the borrower towards more suitable options.

Assessment of linked products or subsidised products

Linkage linkage linkage linkage linkage

The linkage with banks is fundamental, there is a whole series of linked products that bind you closer to the bank and allow you to earn more money. That’s what it’s all about, isn’t it?

But in the end, these linked products make your mortgage more expensive (and sometimes very expensive).

That is why you have to be very attentive to linked products.

I always say that linked products are, in common parlance, the bank has you by the short hairs……..

The term “linked products” has disappeared.

Because it was a bit strong for the bank to force you to take them in order to lower the interest rate of your mortgage.

But they still exist and they are simply now called subsidised products.

The evaluation of linked products is essential when applying for a mortgage.

Many attractive offers may be subject to additional products, such as insurance, alarms, services, etc. It is therefore essential to analyse not only the benefits but also the costs that these may entail.

It is therefore essential to analyse not only the benefits, but also the costs they may entail.

Analysis of insurance and other products linked to your mortgage

Some banks offer mortgages with a priori interesting conditions, but will require you to take out insurance or linked accounts.

It is common for these to be included:

- Home insurance

- Life insurance

- Health insurance

- Savings or current accounts

- Alarm service

It is crucial to assess whether you really need each of these products.

Although they may offer a discount on the mortgage, the additional costs of these policies must be taken into account.

A detailed analysis will be key to understanding whether the initial savings outweigh the costs in the long run.

Impact of tied products on total cost

Linked or modified products can significantly increase the total price of the mortgage.

Essentially, even if a reduced interest rate is obtained, the costs of additional products can cancel out any initial advantage.

For this reason, it is recommended to calculate the total cost of the mortgage, integrating all the associated services, and compare it with offers that do not require linked products.

This breakdown will help to make more informed decisions, ensuring that you choose the mortgage that really offers the best value for money.

Remember that you will no longer have to pay the mortgage expenses, that is to say, you will not have to pay the stamp duty or the notary or the registry, you will only have to pay the valuation of the house. And surely the opening of the loan file or the study of the mortgage.

Relationship with your current bank

This is an aspect that I understand to be fundamental.

Your bank knows you best. Be careful, this does not mean that they will grant you the mortgage.

The relationship you establish with the financial entity can be a determining factor when it comes to obtaining a mortgage.

Maintaining good communication and a solid history with the bank can facilitate the application process and improve the conditions of the loan.

Benefits of applying for a mortgage with your existing bank

Applying for a mortgage with the bank where you are already a customer offers a number of important advantages. These include:

- Mutual knowledge: The bank has access to the customer’s financial history, which can simplify risk assessment.

- Preferential terms: Banks can often offer more favourable terms to their regular customers, such as reduced interest rates.

- Ease of processing: Being already linked to the bank can speed up the processing of the mortgage application.

How to improve your relationship with the financial entity

Strengthening your relationship with the bank is key to benefiting from better offers and preferential treatment. Some strategies to achieve this are:

- Use multiple services: Signing up for additional products such as savings accounts, credit cards or insurance can strengthen ties with the institution.

- Make timely payments: Meeting financial obligations in a timely manner demonstrates responsibility and commitment.

- Effective communication: Maintaining good communication with bank advisors and resolving questions when they arise can enhance the relationship.

The documentation required for the mortgage application process is critical.

Having all the required documents will facilitate loan approval and reflect good organisation on the part of the applicant.

Documentation required for the mortgage application process

I am convinced that speed and agility in the delivery of the document is important.

Let’s be serious, nobody decides overnight to take out a loan. Indeed

Taking out a mortgage is a decision that comes from a long time ago and you have to prepare yourself very well even in the long term.

That is why, when you decide to ask for a loan from a bank, you should be prepared to have all the documentation and not take too long to get it and give it to the bank.

List of documents you should have ready

Before starting the application, it is crucial to gather the documentation that the bank will require.

Here are some of the most common documents that are usually requested:

- Official identification (DNI or NIE).

- Proof of income, which may include

- :Pay slips for the last three months.

- Income tax returns for the last two years.

- Company certificates if you are an employee.

- Latest tax returns for the self-employed, such as VAT (form 303), payment in instalments (form 130).

- Bank statements for the last three or six months.

- Information on existing debts, such as personal loans, leasing, renting or credit cards.

- Title deed or rental contract, if applicable.

- Certificates of no tax or social security debts.

- An employment record for foreigners, certificate of tax residency.

- Any other additional documents that the bank may require.

Not being on the list of defaulters is essential for them to give you the mortgage.

In this idealista article you will find out how to find out if you are on the list of defaulters.

Finally how to deal with bank refusal and how to improve

Failure is the order of the day.

But in reality it has existed all our lives.

Remember, the one who succeeds is the one who always gets back up.

The new science of resilience is the one that allows you to adapt to the situation, changing your position according to the existing factors.

Failure is a factor that is always present. But being turned down for a mortgage is not failure.

Receiving a rejection on a mortgage application can be discouraging.

However, it is essential to understand the reasons behind this decision and take steps to improve the chances on future applications.

Common reasons for mortgage rejection

There are several reasons that can contribute to a bank’s refusal of a mortgage.

Among the most common are:

- Poor credit history scores.

- High levels of debt relative to income.

- Insufficient savings to cover down payment and additional expenses.

- Lack of employment stability, such as a temporary contract or irregular employment history.

- Errors in the documentation submitted.

Strategies to improve your chances after a rejection

If you receive a rejection, there are several strategies you can follow to improve the situation. The following are some of the most effective:

- Request a detailed report from the bank explaining the reasons for rejection.

- Review and correct errors in credit history through corrective actions.

- Reduce existing debts before reapplying for a mortgage.

- Increase savings, with the aim of presenting a better initial repayment capacity.

- Consider obtaining a guarantor who can support the application.

Implementing these actions can open up new opportunities, making it easier to get approved for a mortgage in the future.

Recommendations

You have to be honest with yourself.

Society forces us to raise a family, to work, to spend, to consume and, of course, to take out a mortgage.

Are you willing to sacrifice or do you prefer to live well?

Are you willing to follow society’s guidelines?

Many young people have decided to stand up and say NO. And I see it as a good thing.

Living well means not having too many burdens, too many responsibilities, too many commitments.

Paying a mortgage is a burden for life and now you may have a lot of energy, a lot of desire to work but you have to think long term.

Why having a mortgage is a big responsibility and a big expense.

I have a mortgage, a wife and three children and I recognise that couples who live in rented accommodation and have a dog seem to me to be smarter than me.

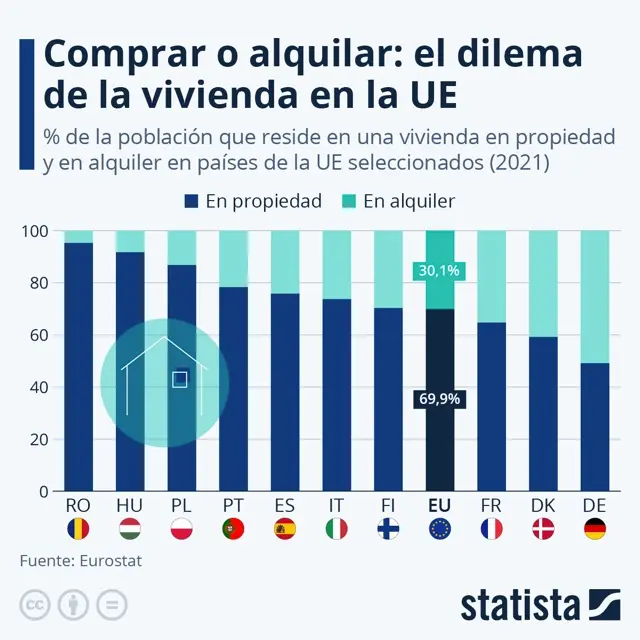

In Spain the idea of being an owner is very deeply rooted, but more and more renting is gaining ground because being a tenant gives you freedom.

Beware of choosing a fixed or variable rate mortgage.

This detail I think is a function of each person, of their way of being, of their aversion to risk because in the end the bank makes money with both options.

Be nice to the bank staff

I insist, kindness leads you to achieve all your goals in life.

Choose the right time to take out your mortgage

You have to be aware of the bank’s situation. There are many times when banks fight for mortgages and that is where you can benefit.

Prepare in advance

If you are self-employed, prepare yourself a year or two in advance, increase your income, control your expenses and save as much as possible.

If you have a salary, it is difficult for you to increase your income, you have no choice but to save and reduce your lifestyle.

The bank will always benefit, because it is designed to make money.

Don’t forget that.

Patrick Gordinne Pérez

Graduate in Economics from the University of Alicante