")

The Beckham Law, commonly known as the “Ley Beckham” or Spanish impatriate regime, introduced in 2005, establishes a special tax regime to attract international talent to Spain.

It offers significant tax benefits to seconded workers, facilitating their integration into the Spanish labour market.

This regulatory framework aims to stimulate the economy and encourage the growth of emerging sectors in Spain.

Over the years, it has undergone a number of reforms, adapting to the new needs of the global labour environment.

What is the Beckham Law?

The Spanish legislation known as the Beckham Law has been designed as an instrument to attract foreign talent to the country, providing significant tax benefits for those who relocate for work purposes.

Definition and Origin

The Beckham Law, formally known as the special regime for posted workers or special impatriate regime, was enacted in 2005.

It is named after the famous footballer David Beckham, who was one of the first to benefit from this regime when he moved to Spain to play for Real Madrid.

This regulation was established in a context in which Spain was seeking to revitalise its economy and attract foreign investment, particularly in emerging and high-skilled sectors.

The law has undergone numerous changes and updates over the years, one of the most notable being the enactment of the Start-Ups Law in 2022, which modified certain aspects to make it more accessible and relevant to foreign workers.

Objectives of the Beckham Act

The main purpose of the law is to attract highly qualified professionals, entrepreneurs and investors to Spain. Through a favourable tax regime, it seeks to promote job creation and economic growth. Specific objectives include:

- Promote the incorporation of international talent in strategic sectors.

- Facilitate the creation of companies and investment in the country.

- To increase the competitiveness of the Spanish economy at a global level.

Importance in the Tax Context

The Beckham Law has played a crucial role in shaping the tax system for posted workers in Spain. Its attraction lies in the possibility of being taxed at a fixed and reduced tax rate compared to the progressive rates applicable to ordinary residents. Among its main features, the following stand out:

- The limitation of taxation only to income generated within Spain.

- Exemption from taxation on income earned abroad, thus promoting a favourable environment for international talent.

- Its importance in the European context, where many countries have started to adopt or adapt similar legislation to attract high-value professional profiles.

The tax regime for inpatriates allows non-residents who travel to Spain to work to choose to pay tax as non-residents instead of personal income tax.

This, during the tax period in which they change their tax residence and in the following five years.

Requirements for applying the Beckham Law

To benefit from this tax regime, it is necessary to comply with certain specific requirements that ensure correct application.

These requirements are aimed at defining who can benefit from the tax advantages offered by the regulations.

Tax Residency

One of the fundamental requirements to benefit from the special regime is tax residence.

To be eligible for the Beckham Law, the applicant must not have been a tax resident in Spain during the five tax years prior to the year in which they move to the country.

This limit has recently been reduced from ten to five years, making it easier for more professionals to benefit from the scheme.

Beckham Law Working Conditions

It is essential that the applicant has a formal employment relationship in Spain that supports their acceptance of the Beckham Law.

Until December 31, 2022

This implies that they must have a new employment contract in the country.

Alternatively, you may be appointed as a director of an unrelated entity or submit a letter of displacement from the company attesting to your transfer.

Examples of Working Conditions

- Direct hiring in a Spanish company.

- Appointment as a director or manager of a legal entity in the country.

- Posting by a foreign company with activities in Spain.

From January 1, 2023

- As a result of an employment contract.

- As a result of the acquisition of the status of director of an entity.

- As a result of carrying out an economic activity in Spain classified as an entrepreneurial activity.

- As a result of the performance in Spain of an economic activity by a highly qualified professional who provides services to emerging companies.

Prohibition of Permanent Establishment

Applicants who wish to benefit from the Beckham Law must meet the requirement of not having (in the past) generated income through a permanent establishment in Spain.

This implies that they cannot have an autonomous activity that provides them with income in the country, which seeks to prevent the regime from being used as a tool for tax avoidance.

Permanent Establishment Considerations

- It is not allowed to have a commercial premises or physical headquarters in Spain that generates income.

- Income must come exclusively from wages or other forms of labor remuneration related to work in the country.

Compliance with these requirements is essential to be able to benefit from the advantageous conditions offered by this tax regime, and to ensure that the objective of attracting international talent is effectively met.

This regime can now be applied to many more persons, such as administrators with more than 25% of the capital, all teleworkers, entrepreneurs, highly qualified self-employed and even family members of the impatriate.

Beckham Act Tax Benefits

The Beckham Law offers multiple tax benefits that are attractive to professionals who decide to relocate to Spain.

These factors favour the integration of qualified workers and entrepreneurs, facilitating their adaptation to the Spanish economic environment.

Special Tax Regime

The Special Tax Regime that applies to beneficiaries of the Beckham Law is one of its main attractions.

This regime allows taxpayers to be taxed as if they were non-residents, which means that they are only liable to pay tax on income generated in Spanish territory.

This provision is particularly advantageous for those workers who have income abroad, as they can keep their wealth out of Spanish tax reach.

24% Flat Tax Rate

One of the highlights of the Beckham Law is the flat tax rate of 24%.

This tax regime applies to the first 600,000 euros of income, which represents a significant reduction compared to progressive tax rates that can exceed 50% for other taxpayers.

This favourable structure allows posted workers to keep more of their income, thus incentivising their decision to reside and work in Spain.

Beckham Law Exemptions and Deductions

The Beckham Law also provides for a number of exemptions and deductions that further enhance its tax attractiveness. Among the most relevant are:

Income in Kind.

Income in kind, such as employer-provided health insurance or employer-provided food expenses, is exempt from taxation.

This results in significant savings for beneficiaries, as they are not obliged to include these benefits as part of their taxable income.

Elimination of Form 720

Taxpayers under this regime are not required to file Form 720, which is the form used to declare assets abroad.

This exemption reduces the administrative burden and simplifies tax management for beneficiaries.

Limited taxation

By limiting taxation only to income produced within Spain, posted workers can avoid the tax impact of their international income.

This feature is particularly interesting for those with multiple sources of global income.

Beckham Act Application Procedure and Documentation

The process of applying for the special regime involves a series of steps and the submission of specific documentation to the Tax Agency. The essential stages of this procedure are detailed below.

Formal Beckham Act Application

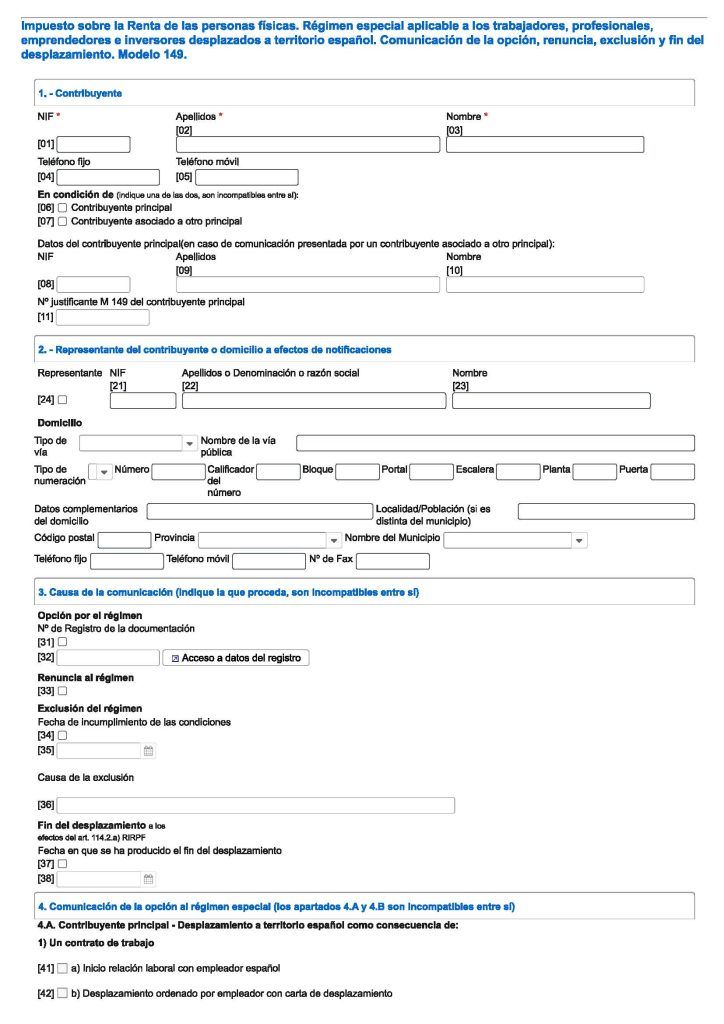

To start the application process, you need to submit a formal application throughform 149.

You will need a digital certificate. Read our article What is a digital certificate for?

This declaration must be made by the interested party or their representative and must reflect compliance with all the requirements established by the corresponding regulations.

The application can be made electronically through the Tax Agency’s electronic headquarters, thus ensuring more agile and efficient management.

It is essential that the application is duly completed and that each section is completed accurately to avoid possible delays or refusal of the scheme.

Documentation Required for the Beckham Act

The documentation required to formalise the application includes several key documents. The main requirements are listed below:

- Proof of Previous Residence: A document accrediting that the applicant has not been a tax resident in Spain for the five years prior to the application.

- Employment Contract: It is essential to present the signed contract proving the employment relationship in the country, as well as the duration and conditions of the contract.

- Letter of Displacement: For those who move for work purposes, a letter from the company confirming the displacement and the specific circumstances of the same is required.

- Identity Documents: Copy of the applicant’s ID card or passport, together with any other identification document that may be requested by the Tax Agency.

- Proof of No Permanent Establishment: Documentation accrediting that the worker does not have a permanent establishment in Spanish territory.

Deadlines and Reviews by the Tax Agency

Once the application and the required documentation have been submitted, the Tax Agency proceeds to a thorough review.

This process can take varying amounts of time, but generally, decisions tend to be issued within 10 working days.

It is important for applicants to be aware that they may receive additional requests for documentation or complementary information during the assessment process.

If necessary, the Tax Agency will request such information through the platform where the application was submitted.

At the end of this period, the Agency will notify the interested party whether the application has been approved or rejected.

If it is accepted, the taxpayer will start to benefit from the special tax regime from the start of their employment activity in Spain or from the date of the application, as stipulated in the approval.