")

Payrolls are essential documents in the employment relationship between an employee and his or her company or employer, as they detail the salary and deductions applied to workers. These receipts are essential to ensure compliance with labour and tax obligations. Understanding the structure of a payslip is fundamental.

Through its different parts, it is possible to know the employee’s net remuneration, as well as the contributions made to Social Security and tax withholdings.

What is a payroll?

This document is fundamental in the employment relationship, as it reflects the economic perceptions that a worker receives for his or her professional activity. It is issued monthly and is a record that details, among other aspects, the corresponding salary and the deductions applied.

A payslip includes several key elements that allow both the employee and the employer to have a clear view of remuneration and tax obligations. It is more than a mere receipt; it acts as a proof before labour and tax authorities.

It contains a breakdown of the amounts that the employee receives, as well as the social security contributions and other withholdings. This information allows the worker to know his or her gross salary, which is the amount before deductions, and the liquid to be received, which is the final amount received after subtracting the relevant deductions.

Parts making up the payroll

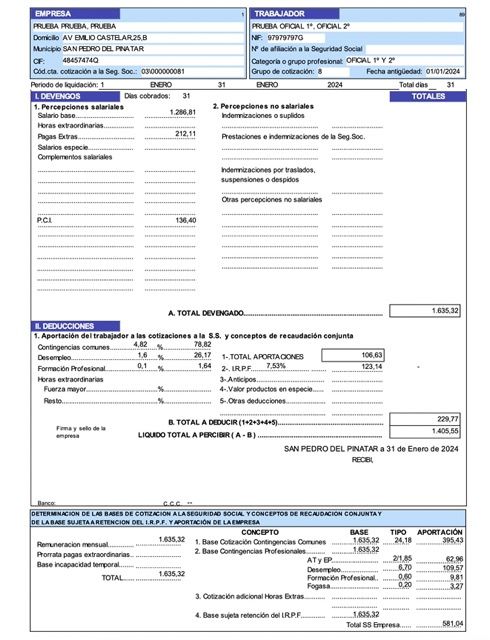

The payroll is structured in different sections that guarantee the correct information on the employee’s payments and deductions. Below is a breakdown of the essential parts that make up this document.

Header

The header is the initial part of the payslip, where fundamental data is included to identify the company and the worker. This section sets the context, facilitating the understanding of the rest of the document.

Company details

In this subsection, the details of the company making the payment are reflected. Typical details are:

- Company name: Official name of the company.

- Address: Physical location where the company is located.

- CIF (Tax Identification Code): Number that identifies the company for tax purposes.

Social Security contribution account code: Identifier for - Social Security affiliation.

Worker’s details

This part must contain the employee’s personal information, which includes:

- Name and surname(s): Identification of the employee.

- DNI: National Identity Card of the employee.

- Social Security affiliation number: Number that allows access to the benefits of the system.

- Professional category: Definition of the position held in the company.

- Length of service in the company: Length of time working in the organisation.

It is essential to include the corresponding settlement period, which is usually monthly.

Earnings

Payments represent all the financial payments that the employee receives during the period. This part is broken down into salary and non-wage payments, each with specific elements.

Salary payments

Wage and salary payments are those that are part of the gross salary and are divided into:

- Basic salary: Amount fixed for the work carried out in the corresponding period.

- Wage supplements: Supplements to the basic salary due to concepts such as seniority, night work or dangerousness.

- Overtime: Additional remuneration for work carried out outside the established working hours.

- Overtime payments: Additional payments that are normally distributed throughout the year.

Non-salary payments

This category includes other types of income that do not form part of the regular salary, such as:

- Per diems: Compensation for subsistence expenses during travel.

- Transport expenses: reimbursements for work-related travel.

- Allowances: Payments that may be received in the event of damage or injury.

- Social security benefits: Subsidies that the worker receives from the Administration.

Deductions

Deductions are the deductions that are applied to the gross salary to determine the employee’s net salary. They include tax and social security obligations.

Social security contributions

This section includes contributions made by the worker to the social security system. Contributions are crucial to ensure access to services such as health care and pensions. Rates may vary according to the category and type of contract of the employee.

Personal income tax withholdings

IRPF is the personal income tax that is withheld from an employee’s salary. The amount to be withheld depends on different factors, such as the gross salary, the employee’s personal and family situation, as well as the tax regulations in force.

Other deductions

There may be other deductions applicable that are not directly related to Social Security or IRPF. These may include:

- Advances: Amounts that the employee has previously claimed.

- Garnishments: Deductions for debts that the employee may have.

- Loans: Deductions for loan repayments previously granted.

Liquid to be received

The cash to be received is the final amount that the employee will receive in his or her bank account. It is calculated by subtracting the total deductions from the payments. This is the net salary actually paid to the employee and is vital for your financial planning.

Social security contribution bases

This section defines the amount of the contribution base for common contingencies, professional contingencies, unemployment and pension. It also defines what the company contributes to social security.

In English, this is the basis for what you will receive if you have an accident at work, become ill, are dismissed or retire.

Payroll types

There are different types of payroll that are adapted to the characteristics of the employee and the company’s policies. They can be classified according to the periodicity of payment, the type of personnel and the special circumstances surrounding each employee.

According to the periodicity of payment

The periodicity with which wages are paid can vary. From weekly to monthly payments, each method has its own context and prevalence depending on the employment sector.

Weekly payrolls

Weekly payrolls are less common compared to other payment frequencies. It is often used in temporary jobs or those occupations with a high turnover of staff. This type of payroll allows the worker to be paid more frequently, which can be beneficial for those with immediate financial needs.

Bi-weekly payrolls

Bi-weekly payrolls are a middle ground between weekly and monthly payrolls. They are generally used by companies in different sectors that prefer to pay in 15-day periods. This is a less common option, but also helps to improve the employee’s liquidity.

Monthly payrolls

Monthly pay slips are the most common in Spain. They are usually drawn up at the end of each month and reflect a summary of the income and deductions accrued in that period. This format is favoured by most companies, as it simplifies administrative management and allows for predictability in accounting.

Depending on the type of personnel

The classification by type of personnel focuses on the positions occupied by the employees within the company. This distinction is essential to determine the wage treatment and the specific conditions of each group.

Senior managers

Senior payrolls include managers and executives who tend to have a more complex salary package. Often, this type of payroll incorporates bonuses, incentives and other benefits that are not common for general staff. The preparation of these payslips requires special attention because of the variables that influence remuneration.

General staff

General staff refers to the rest of the company’s employees. Their pay slips are generally more standard, reflecting the basic salary and related allowances. This type of payroll covers the majority of employees and is managed according to common labour regulations.

For special circumstances

Some work situations require special payroll processing. These circumstances may include overtime, overtime pay and sick leave, the regulation of which must be respected to ensure that the worker receives what he or she is entitled to.

Overtime is the time an employee works beyond his or her regular hours. On the payroll, this additional time is accounted for and paid at a higher rate than usual. The regulations set limits on the amount of overtime a worker can work and the conditions under which it must be paid.

Pro-rata overtime payments

Overtime payments refer to additional income given to workers, such as holiday or Christmas bonuses. Sometimes these payments may be pro-rated during the year, spread over regular payroll months. This approach allows employees to receive a more consistent income throughout the year.

Time off work

When an employee is on sick leave, their payroll is adjusted to reflect this. Depending on the duration and reason for the leave, different calculation and deduction criteria apply. Current legislation establishes how payrolls should be handled in such scenarios to ensure that the employee’s rights are respected.

Regulations on the delivery of payslips

Payroll regulations are essential to regulate the relationship between employers and employees. These laws impose obligations on companies with the aim of ensuring transparency in remuneration and compliance with labour rights.

Employer obligations

The employer has the duty to draw up and deliver the pay slips to his employees in a timely manner and in accordance with the regulations in force. This obligation includes essential aspects that must be considered:

- Drawing up pay slips on a monthly basis or as agreed, respecting the established deadlines.

- Provide clear and detailed information on salary, and a breakdown of deductions applied.

- Keep a record of pay slips submitted as proof of compliance.

Failure to comply with these obligations may result in financial penalties and repercussions on the employment relationship with employees.

Submission format

The regulations allow for different forms of delivery of payslips, adapting to the needs and preferences of both the company and the employees. The most common formats are:

Physical format

The physical format of the payslip has traditionally been the most commonly used. It is delivered on paper and must meet certain presentation requirements:

- Clearly visible names and details of the worker and the company.

- A clear and numbered breakdown of payments and deductions.

- Signature of the person in charge of the company or a suitable seal that guarantees the veracity of the document.

This format allows employees to have a tangible document that they can keep for their personal records.

Digital format

The use of digital formats has been increasing, supported by the digitisation of companies. Payroll can be sent via email or through specific human resource management platforms. Features include:

- Immediate access to payroll from any device, providing ease and convenience.

- Reduced paper usage, encouraging a more sustainable practice.

- Ability to store and manage payroll in an orderly and efficient manner.

Regardless of the format chosen, it is crucial that the employee has access to their payroll in a timely manner, ensuring clarity and transparency in all information related to their salary.

Payroll management tools

There are many tools that make payroll management easier for both large and small and medium-sized companies.

These technological solutions make it possible to automate processes and ensure compliance with labour and tax regulations.

Human resources software

Human resources software is an essential tool for comprehensive payroll management. This type of software offers multiple functionalities that help simplify tasks related to personnel administration.

- Employee management: Allows you to store and manage the information of each employee, including personal data, employment contract, seniority and other relevant aspects.

- Automatic calculation: Facilitates the calculation of payroll, considering different variables such as hours worked, withholdings, and perceptions. This reduces the risk of manual errors and saves time.

- Integrated accounting: Integrates payroll management with company accounting, allowing more effective tracking of labour expenses and ensuring that withholdings are correctly accounted for.

- Reporting and statistics: Generates detailed reports to assist in strategic decision making, as well as in complying with tax and labour obligations.

Payroll platforms

Payroll platforms are specific tools that focus on the processing of workers’ economic data. They aim to facilitate the calculation of salaries and ensure compliance with applicable regulations.

- User-friendly interface: These platforms usually have an intuitive design, allowing users to perform calculations quickly and easily, without the need for advanced accounting knowledge.

- Automatic updates: They are regularly updated with changes in labour and tax legislation, ensuring that payrolls are calculated in accordance with current rates and regulations.

- Online access: Many of these tools are accessible in the cloud, allowing users to manage payroll from any location and device with an internet connection.

- Integrations with other systems: They are commonly integrated with other systems used in the company, such as accounting or human resources management software, increasing the efficiency of information management.

Payroll accounting: Step by step

Payroll is a fundamental process in human resources management. It consists of a series of steps that ensure that employees are properly compensated for their work, in compliance with all legal regulations. The key steps in carrying out this process are described below.

Information gathering

In this initial phase, all necessary information related to the employee and his or her employment status must be collected. This information includes:

- Personal details of the employee, such as first name, surname and ID number.

- Details of the employment contract, including start date, type of contract and working hours.

- Information on applicable salary payments, such as basic salary, allowances and overtime.

- Details of applicable deductions, such as social security contributions and income tax withholdings.

- Special conditions, such as absences, sick leave and overtime payments.

Calculation of payments

Once the information has been collected, the accruals are calculated. Payments are divided into salary and non-wage payments (at this stage it is essential to have the applicable collective agreement):

Wage payments

- Basic salary: This is the amount agreed for the provision of the service during the corresponding period.

- Wage supplements: These include additional concepts to the basic salary, such as seniority, night work, dangerousness, etc.

- Overtime: This represents remuneration for time worked beyond the agreed working hours.

- Overtime payments: These can be prorated throughout the year or can be paid on certain dates.

Non-wage payments

Non-wage payments cover expenses that can be reimbursed by the employer, such as:

- Subsistence and travel expenses.

- Severance pay or relocation allowances.

- Social security benefits, if applicable.

Calculation of deductions

After calculating the total payments, the next step is to determine the deductions to be applied to the payroll. These deductions are essential to comply with tax and social security obligations:

Social Security contributions

This refers to the amounts that the employee must contribute to access services such as health, pensions or unemployment.

Personal income tax withholdings

- Personal income tax is withheld according to current tax regulations and the employee’s personal circumstances.

Other deductions

- These may include advances, garnishments, or specific agreements that affect the employee’s payroll.

Payroll preparation

Once both payments and deductions have been calculated, the payroll is prepared. This document must comply with current regulations and be transparent to the employee. It must ensure that:

- Company and employee data are clearly presented.

- Payments, deductions and the liquid to be received are correctly detailed.

- The design of the document facilitates the understanding of each component of the payroll.

Delivery of the payroll

Finally, the payroll must be delivered to the employee. This step is crucial and must be done at the agreed time, normally at the end of the month. The forms of delivery can be:

- Physical format: Printout on paper that the employee receives directly.

- Digital format: Sending by e-mail or through a digital management platform, thus ensuring immediate access and easy consultation.

The delivery of the payroll should be accompanied by a communication explaining any aspect that could be confusing for the employee, thus promoting transparency in the employment relationship.

Aspects to consider when calculating the payroll

Payroll accounting requires attention to various factors that may influence its presentation and the amount to be paid. The most relevant aspects that must be taken into account during this process are detailed below.

Type of contract

The type of contract a worker has is a fundamental element in the calculation of your payroll. The different types of contract can affect both the wage base and the contributions and deductions. The following types are considered:

- Full-time: Employees with this type of contract work the full number of hours stipulated by law. Their pay slips reflect the full salary without any hourly reductions.

- Part-time: Part-time employees receive a salary proportional to the hours they actually work, which affects the calculation of payments and deductions.

- Temporary contracts: These contracts may have specificities in terms of duration and conditions, impacting on salary payments and the calculation of severance payments if applicable.

- Indefinite contracts: These usually include clauses that benefit the employee in terms of stability, which may have an impact on benefits and other payments.

Personal situation of the employee

The individual circumstances of each employee are a determining factor in the payroll. Factors such as marital status, number of dependents or migration status influence personal income tax withholdings.

- Marital status: Married or cohabiting workers may benefit from a lower withholding under the regulations compared to single workers.

- Number of dependants: Workers with children or dependents are eligible for tax deductions, which affects the amount to be withheld.

Situation of disability: Those who suffer from a disability may have variations in their - Social Security contributions and in the economic perceptions.

Collective agreement

The applicable collective bargaining agreement is a key element in labour relations and can establish specific parameters that affect the payroll. This regulatory framework determines aspects such as:

- Base wage: Agreements may establish a minimum wage applicable to workers in a specific sector, thus guaranteeing a standard of income.

- Wage supplements: These will depend on the sector and may include bonuses for seniority, night work, or dangerousness, which will vary from one agreement to another.

- Working conditions: Aspects such as the length of the working day, leave and rest days are also usually regulated in these agreements.

Sick leave and special payments

Justified absences, such as sick leave, and the treatment of special payments are factors to be considered. Leave of absence may influence the salary to be received, since:

- Temporary sick leave: Workers on sick leave or maternity leave may receive reduced pay during this period. The regulations regulate how this amount should be calculated.

- Extra payments: Depending on the collective agreement, extra payments may be prorated during the year, which will influence the total amount that appears on the monthly pay slip.

Frequently asked questions about payroll

Payroll FAQs address the most common questions that may arise for both employees and employers.

These queries help to clarify essential aspects of payroll and how it works in the workplace.

What is included in a payroll?

A payslip includes several key elements that allow the employee to know the details of his or her remuneration. These are:

- Employer and employee details: Identification of the company and the worker, together with the professional category and the pay period.

- Payments: All the financial payments received by the employee, divided into basic salaries, salary supplements, overtime and overtime payments.

- Deductions: Social Security and Personal Income Tax deductions, as well as advances or any other corresponding deductions.

- Cash to be received: The final amount that the worker will receive in his/her bank account after all deductions have been applied.

How are deductions calculated?

Payroll deductions are calculated taking into account several factors. The main deductions include:

- Social Security contributions: This amount is determined according to the worker’s gross salary and the regulations in force relating to health, pensions and unemployment.

- Personal income tax withholdings: Income tax withholding is calculated considering the gross salary, the worker’s marital status and any dependent children or dependents.

- Other deductions: These may include advances, payments for garnishments, or any other deductions agreed between the employer and employee.

What to do if I do not receive my paycheck?

If an employee does not receive his or her paycheck, certain steps must be taken to resolve the situation. It is important to act quickly and clearly. The actions to consider are:

- Contact the human resources department: This is the first step to take to confirm if there was an error in the payroll process.

- Review the employment contract: It is essential to check that both the payment and the frequency of payment are in accordance with the contract.

- Register the complaint: If the problem persists, a written complaint should be made to the company, recording the situation.

- Consult a labour lawyer: In complex situations, it is advisable to obtain legal advice to ensure that labour rights are being respected.

PAYROLLS SESPA, SAS y GVA

Payrolls in the SESPA, SAS and GVA organisations have specific characteristics that differentiate them from other modalities.

It is important to understand how they are structured and what particularities accompany them in each of these cases.

The details relevant to each system are set out below.

Specificities of SESPA payrolls

The SESPA (Employment and Training Service) payrolls have several specificities that point to the regulation of contracts within multiple sectors. The most salient elements are:

- Frequency of payments: Generally, payrolls in SESPA are managed on a monthly basis, but there may be special contracts that regulate other frequencies.

- Specific allowances: Depending on the type of contract, allowances for seniority, training or specialisation may be added, which are decisive in the gross salary.

- Special deductions: Personal income tax deductions may vary depending on the tax regime to which employees belong, influenced by their family and personal situation.

Special features of SAS pay slips

The SAS (Andalusian Health Service) has a very structured regulatory framework that affects its payrolls. Among the most relevant features are:

- Staff classification: SAS payrolls are divided into different categories, from health care staff to administrative staff, which may influence the salary structure.

- Extraordinary payments: SAS professionals usually receive two extraordinary payments per year, which are added to the gross salary, significantly increasing the annual salary.

- Bonuses and bonuses: Bonuses may be included for shift work, night work or other circumstances that guarantee a salary in accordance with the requirements of the post.

Characteristics of GVA pay slips

Pay slips in the GVA (Generalitat Valenciana) have characteristics that reflect the regulations in force at the regional level. The most important aspects are:

- Treatment of public employees: The contracts of public employees are strictly regulated, respecting agreements and legislation specific to the public administration.

- Adjusted deductions: Salary deductions are adapted to regional tax regulations, which may differ from those applied by private entities.

- Promotion and training: There is a focus on staff promotion and continuous improvement of their training, which may be reflected in salary increases and bonuses.

The influence of collective bargaining on pay slips

A collective agreement is an agreement that sets out the terms and conditions of employment between employers and workers within a specific sector or company.

This document has a significant impact on payrolls as it regulates various aspects affecting pay and working conditions.

Areas where collective agreements can influence payrolls include:

- Minimum wage: This establishes the minimum wage that workers must receive, which in no case may be lower than that stipulated by the collective agreement.

- Wage supplements: Defines different supplements that employees may receive, such as seniority, hazard or transport bonuses.

- Extraordinary payments: Regulates the frequency and amount of additional payments, such as summer or Christmas bonuses, and whether these are prorated throughout the year.

- Working hours and working time: This indicates the length of the working day and how overtime is to be remunerated, which directly affects payroll payments.

- Mobility aspects: This may include conditions on transfers or job changes, which also impact on financial compensation.

Compliance with the provisions of the collective agreement is mandatory for companies. This ensures that workers are treated fairly and that their pay reflects the agreed conditions.

If any company fails to comply, it can face legal sanctions and negative repercussions on the employment relationship.

Periodic review of collective agreements is also important.

As economic and employment circumstances change, it is essential that agreements are updated to adapt to new realities and needs.

This may include annual reviews or reviews every few years, depending on the regulations in force in each sector.

Consequences of non-compliance with payroll regulations

The consequences of non-compliance with payroll regulations can have a significant impact both financially and on the employer-employee relationship. Violations can vary in severity and impact on multiple aspects of the organisation.

Fines and penalties

Payroll non-compliance can result in financial penalties that directly affect the company. These fines are imposed by the relevant labour and tax authorities and can vary depending on the severity of the violation. Financial consequences include:

- Financial penalties: Sanctions can range from small penalties for administrative errors to significant fines for serious non-compliance, such as failure to submit payslips or errors in deductions.

- Regularisation requirements: The authorities may require the company to correct the anomalies detected, which may involve the payment of amounts owed to employees and the regularisation of social security contributions.

- Interest on late payment: In the event of late payment, companies may face the obligation to pay interest for the time that has elapsed since the date on which the amounts were due.

Impact on the employment relationship

Non-compliance not only results in financial penalties, but can also deteriorate the relationship between employees and the company. Trust is a key element in the employment relationship, and its erosion can have different consequences:

- Staff demotivation: Payroll irregularities can generate dissatisfaction among employees, affecting their morale and motivation. This can lead to lower productivity and deterioration of the working environment.

- Labour disputes: Lack of regulatory compliance can lead to conflicts between employees and management, which could lead to legal claims or strikes.

- Loss of talent: Dissatisfied employees may choose to look for new job opportunities, resulting in high staff turnover and financial losses for the company in terms of training and adaptation of new employees.