")

Form 202 is a tax return used by Spanish companies to make instalments of corporation tax.

It is an advance payment of corporation tax.

Its purpose is to facilitate compliance with tax obligations throughout the financial year.

This form is compulsory for entities that exceed a certain turnover or have achieved a positive result in the previous financial year.

It is essential to know how it works and the filing deadlines in order to avoid penalties.

Definition and Purpose of form 202

This form is a key tool in the tax field for calculating and filing advance payments of corporate income tax.

What is Form 202?

Form 202 is a declaration and self-assessment form that allows companies to make payments in instalments on account of Corporation Tax.

This obligation falls on those entities that, at the end of the previous tax year, have recorded a positive result in the Corporate Income Tax.

It is considered an advance payment that is deducted in the annual corporate income tax return IS declared with Form 200.

This model does not only cover large companies, but also extends to some small and medium-sized companies that meet the necessary conditions.

It is a mechanism that ensures that companies contribute in an orderly and fractioned manner to their tax burden, thus facilitating tax planning throughout the year.

Purpose of instalment payments

The purpose of making these instalment payments is to avoid companies facing a single high tax liability in the corporate income tax that is declared every 25 July of the following year.

Instead, through the Form 202, entities can face their tax burden in a staggered manner, which entails several advantages:

- Improved financial management, given the lower variations in liquidity.

- Facilitation of control over the tax debt accumulated throughout the year.

- Prevention of tax surprises at year-end, allowing companies to better plan their resources.

This mechanism also serves to maintain a good relationship with the Tax Agency by demonstrating a proactive and responsible attitude in complying with tax obligations.

Parties obliged to file Form 202

Compliance with tax obligations is essential for companies in Spain. Below is a list of the parties obliged to file Form 202, as well as the specific conditions that determine this obligation.

General Filing Conditions

The filing of Form 202 is compulsory for several entities whose tax behaviour is governed by Corporate Income Tax. This obligation applies to taxpayers that meet certain criteria established by current tax regulations. The main points to consider are set out below:

- Legal entities operating as trading companies.

- Entities which, although they are not companies, are subject to corporate income tax on account of their economic activities.

- Organisations which, although not for profit, generate income and have associated tax obligations.

Specific Cases of Obligation

Within the general conditions, there are specific cases that determine the obligation to file Form 202. These are organised around criteria of turnover and economic results obtained in previous years.

Turnover in excess of 6 Million Euros

Companies whose turnover exceeds 6 million euros in the previous tax year are obliged to file Form 202. This limit is established to ensure that larger entities maintain an adequate tax contribution and make their tax payments in accordance with the legislation. The criteria for calculating the volume are based on the total income earned in the previous year and correct accounting is essential to comply with this obligation.

Positive Result in the Previous Year

Even if the turnover is less than EUR 6 million, entities that have obtained a positive result in the previous year are also obliged to file this form. This condition ensures that all entities that generate profits contribute proactively to sustaining the tax system. Thus, it seeks to promote equity and compliance with tax obligations among all taxpayers, regardless of their size or type of activity.

Deadlines for filing Form 202

The deadlines for filing Form 202 are essential for compliance with tax obligations.

They are established on a quarterly basis, allowing entities to make instalment payments of Corporate Income Tax in an organised and planned manner.

Annual Filing Calendar

The calendar for filing the Form 202 is designed to facilitate compliance with tax obligations at three key times throughout the year.

These deadlines are specific and must be strictly adhered to in order to avoid surcharges or penalties for delays.

Only 3 instalments of form 202 are payable

First payment in April

The first payment corresponding to Form 202 must be made between 1 and 20 April. This period covers the first quarter of the tax year and represents the first opportunity for entities to make their contribution on account of the tax.

Second Payment in October

The second filing deadline runs from 1 to 20 October. In this case, the payment refers to the third quarter of the year, and it is essential that companies comply with this temporary requirement in order to keep their tax situation up to date.

Third Payment in December

The last payment of Form 202 is made between 1 and 20 December. This deadline closes the instalment payment cycle for the year, allowing entities to adjust their final contribution before the annual corporate income tax return.

Rules for the calendar year

The rules for filing the Form 202 follow a calendar year scheme, which means that all instalment payments are concentrated in these three months over the calendar year.

This format simplifies tax planning for companies and ensures harmonised tax reporting.

Deadlines for filing Form 202 other than the calendar year

If your company’s tax year does not coincide with the calendar year, you should take special care when identifying your corporate income tax instalments.

Please note that these payments must always be identified in the same way, regardless of the date on which your company starts its tax period:

- In the “Fiscal year” section appearing on form 202, report the year in which the instalment payment occurs.

- In the “Period” box, always enter the code 1/P for payments in April, 2/P for payments in October and 3/P for payments in December.

Example of form 202 other than calendar year

If your company started its financial year on 1 September 2022, although the payment on account in October will be the first of the financial year, you must indicate that it is the 2P period; and in December, the 3P period.

If you do not comply with this rule (if you identify the October payment on account as 1P and the December payment as 2P, for example), the tax authorities could interpret that your company is submitting instalments for previous periods and impose surcharges that you will then have to appeal.

Process for completing the form 202

The correct completion of the Form 202 is essential to ensure compliance with the tax obligations of each entity.

This process is divided into several key sections that must be completed accurately.

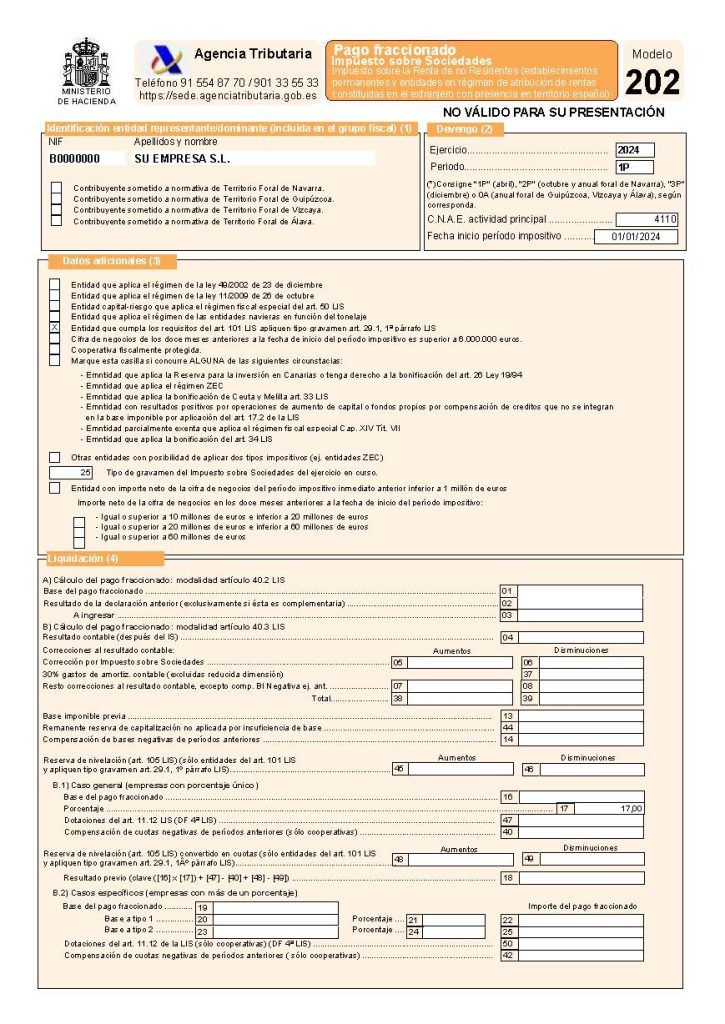

Taxpayer Identification

In this section, it is necessary to enter the basic information of the taxpayer. The Tax Identification Number (NIF) and the name or company name, in the case of legal persons, must be provided.

These data allow the Tax Agency to correctly relate the self-assessment with the taxpayer and avoid possible confusion.

Information on the Tax Period

The tax year to which the return relates must be specified.

This includes indicating the starting date of the tax period and the corresponding type of period, which can be 1P for the first period, 2P for the second, and 3P for the third.

It is also essential to indicate the National Code of Economic Activities (CNAE) that corresponds to the activity carried out by the company, as this allows it to be properly classified in the tax system.

Additional Data Section

This part of the form allows you to provide additional information about the taxpayer’s situation.

It is important to include relevant aspects that may influence the tax return and the tax calculation.

Small Business Status

Entities that are considered small companies, i.e. those with a net turnover of less than 10 million euros, must tick the corresponding box. This condition may affect different types of deductions and allowances to be applied in the tax settlement.

Special Taxation Regime

Entities that are incorporated under a specific regime should also indicate this in this section. This includes non-profit entities, listed real estate investment companies and other categories that may benefit from a particular tax treatment. It is essential that this information is provided accurately to avoid problems in the interpretation of the declaration.

The instalment payment of the year N of the first period 1P (20th April) will probably be different from the instalment payments of the second period 2P (20th October) and third period 3P (20th December).

The instalment payment of the first period 1P is calculated on the tax liability of the year N-2 and the instalment payments of the second and third periods are calculated on the tax liability of the year N-1.

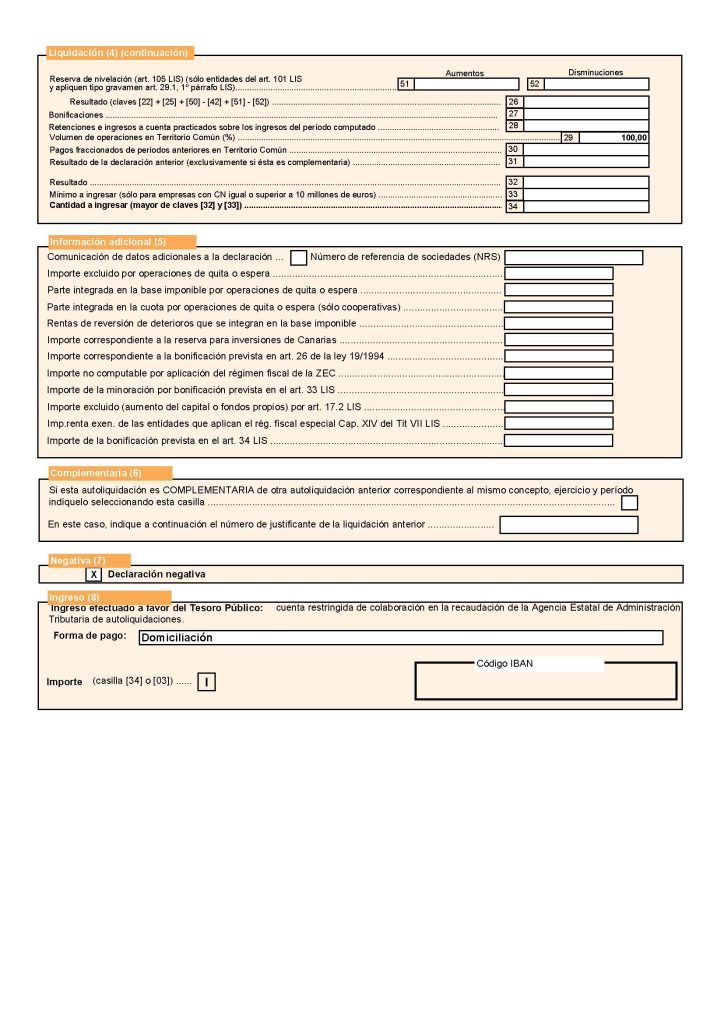

Settlement and Calculation of Instalment Payment

The settlement and calculation of the instalment payment are crucial aspects in the management of Form 202.

- Pay 18% on the taxable income of the previous year.

- Pay 18% on the taxable base of the current year.

Settlement Modalities under the LIS

There are two main methods for the settlement of the instalment payment, each adapted to the different tax circumstances of the obliged entities. The choice of the appropriate modality can have a significant impact on the calculation and management of the payments made.

Article 40.2 modality

This modality is mainly used in the following cases:

- Annual duration: When the last tax period has been annual, the base of the instalment payment is calculated taking into account the full amount of the last corporate income tax return filed. The corresponding deductions, allowances and withholdings are applied to this base.

- Duration of less than one year: For tax periods of less than one year, it is necessary to include the contributions for periods totalling at least 365 days. Special care must be taken if the previous period was the start of the activity, as this calculation modality will not be applicable.

Article 40.3 mode

This option is optional for many entities, although certain organisations are obliged to use it.

Those that decide to opt for this option must file a census return in February of the year in which they wish to apply it.

Calculating the amount of the instalment payments model 202 article 40.3

In general, for tax periods starting in 2024, this percentage is calculated by multiplying by 5/7 the tax rate of the entity, rounded down.

- Companies subject to the general rate 25%: (5/7) × 25 = 17%.

- Small companies 23%: the percentage for calculating the amount of the instalments is: (5/7) x 23 = 16%.

- Newly created companies 15%: in the first tax period in which their taxable base is positive and in the immediately following one, the percentage for calculating the instalments in those periods is 10% (5/7 x 15).

It is essential to be familiar with the conditions surrounding this option due to its complexity.

This option is usually taken if you already know that you are going to have a lower turnover than last year or you have ups and downs with your turnover throughout the year.

Electronic Filing of Form 202

The electronic filing of Form 202 has become an indispensable requirement in a digital environment.

This process is carried out through a specific platform provided by the Tax Agency, which facilitates tax management for entities that must comply with their tax obligations.

Technical Requirements for Filing

Taxpayers must comply with certain technical requirements in order to e-file Form 202 effectively.

These requirements are detailed below:

Obtaining the Electronic Certificate

In order to file the Form 202 electronically, it is necessary to have an electronic certificate.

See this link in our blog What is a digital certificate?

This certificate ensures the authenticity of the declarant and the confidentiality of the information transmitted.

It can be obtained through authorised certifying entities and is essential for accessing the Tax Agency platform.

Verification of the Browser Configuration

Before starting the presentation, it is crucial to verify that the browser settings are appropriate.

Some things to consider include:

- Upgrade to the latest version of the browser to ensure compatibility.

- Adjust the font size and zoom, making it easier to view the form.

- Deactivate pop-up blockers that may interfere with the loading of the platform.

Procedure in the Tax Agency Platform

Once the technical requirements have been met, you can proceed with the filing of Form 202.

The process is carried out in several steps:

- Access the Tax Agency platform using the electronic certificate or Cl@ve credentials.

- Navigate to the section corresponding to Form 202.

- Complete the form with the required information, making sure that all the data is correct.

- Use the ‘Validate’ function before submitting, to detect possible errors or warnings that may arise during submission.

- Once validated, proceed to file the form and obtain the corresponding receipt, which will include the Complete Reference Number (CRN) if applicable.

This procedure must be carried out within the established deadlines, as it is essential for complying with tax obligations within the framework of the regulations in force.

Tips for a Successful Form 202 Return

Correct filing of Form 202 is crucial to avoid problems with the tax authorities.

Below is a series of tips that will facilitate this process and ensure that the return is filed efficiently.

Review and Validation of Input Data

It is essential to thoroughly review all the information before submitting the declaration.

A first step is to use the ‘Preview’ function of the form.

This allows you to detect and correct possible errors in the data entered.

- Confirm that all mandatory fields are correctly filled in.

- Check that the numbers, especially the financial amounts, are accurate and correctly entered.

- Pay attention to the dates and periods selected to avoid discrepancies.

It is very typical to confuse the 3Q quarterly tax return with the 2P instalment payment due in the same period.

Saving and Generating the Complete Reference Number (NRC)

If the result of the tax return is to be paid and you have not opted for direct debit, it is vital to obtain the NRC.

This number is the proof of payment and is required for any subsequent procedures related to the tax return.

- Make sure to keep all documentation supporting both the declaration and the NRC generated.

- Use the ‘Save’ option on the form to prevent loss of information, even if the declaration has not been completed at that time.

Troubleshooting Common Problems and Computer Queries

A number of issues may arise in the course of filing.

Early identification and resolution of these problems is essential to ensure that the declaration is completed successfully.

- If an error occurs when trying to validate the data, check the warning messages provided by the platform.

- Consult the Tax Agency’s help section, where you can find solutions to common problems during electronic filing.

- If the problem persists, do not hesitate to seek professional help or contact the platform’s support to resolve the incident.

Importance and Benefits of the form 202

The correct use of the Form 202 can generate multiple benefits for entities that are obliged to file it.

These benefits are not only related to tax compliance, but also transform the overall management of the company.

Impact on Corporate Tax Management

One of the main benefits of the Model 202 is its contribution to a more orderly and predictable tax management.

Making payments in instalments allows companies to:

- Avoid the accumulation of tax debts at the end of the tax year.

- Spread the tax burden over the year, facilitating financial planning.

- Minimise the impact on cash flow, as payments are made in shorter periods.

This system transforms the way companies manage their tax obligations, leading to a more proactive relationship with the tax administration.

Meeting payments on a quarterly basis can also contribute to a positive assessment by auditing bodies.

Improvements in Financial Assessment and Relations with the Administration

Timely and correct filing of the Model 202 enables companies to be in line with the expectations of the tax authorities, which has a direct impact on the financial assessment.

In this way, the following improvements are achieved:

- Fiscal Reputation: Maintaining a correct self-assessment improves the company’s image in the eyes of the tax authorities.

- Access to financing: Good tax management can be a decisive factor when it comes to obtaining financing, as banks value solvency and compliance with tax obligations.

- Building Trust: Companies that comply with their tax obligations on a regular basis tend to have better relations with the administration, strengthening mutual trust.

Therefore, Model 202 is not only a tax obligation, but also a strategic tool that enhances the effective management of companies and their relationship with the administrative environment.